If you own your own home, housing cost is likely one of your biggest expenses. Housing sure is one of the biggest expenses for our hypothetical million dollar income family. Wouldn’t it be great to be able to lower the monthly mortgage payments?

Housing cost is also one of my biggest expenses. It is second only to income taxes. Therefore, it makes great sense for me to try to lower the mortgage payments as much as possible. I am a big fan of having cash flow, especially if I want to gain financial freedom one day.

Perform Budget Check-up Once A Year

It is a good idea to keep track of your expenses in order to have a handle on where your money goes. This will provide you with the financial information you need if you want to reduce your expenses on a going forward basis.

My advice for you is to perform a budget check-up at least once a year. Review your expenses and then figure out if there are ways to cut your expenses down.

If housing is one of your biggest expenses, just like it is for me, then it makes sense for you to figure out ways to reduce this monthly cash outflow.

Below are 10 ways you should consider in order to lower your monthly mortgage payments.

Way #1: Refinance To A Lower Rate

When the Federal Reserve raises, lowers or leaves unchanged the Federal Funds Rate, it becomes headline news. The whole world is watching the Federal Reserve’s action.

But do you know that the mortgage rate isn’t based off of the Fed Funds Rate? A Fed Funds Rate increase might not result in an increase in the mortgage rate.

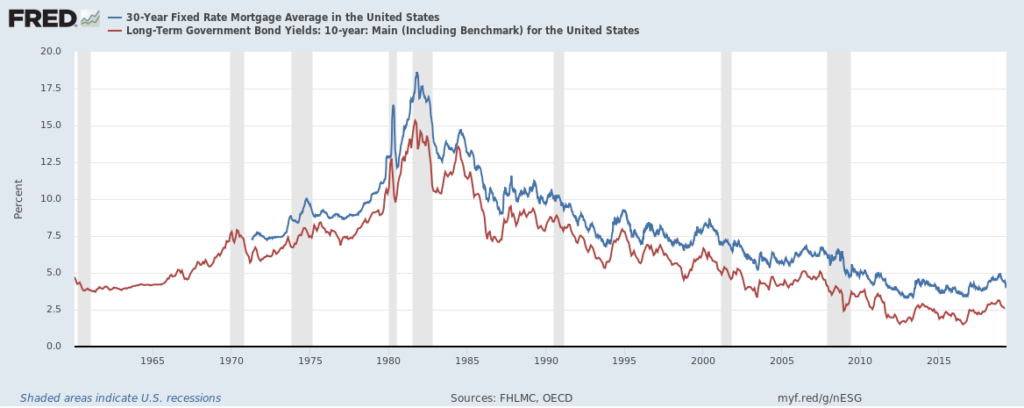

Did you know the 30 year mortgage rate is based off of the 10 year bond yield instead? The 10 year bond yield is what you should be tracking if you want to get a sense of where mortgage rate is heading.

If the 10 year bond yield decreases, the mortgage rates offered by banks decrease. Conversely, if the 10 year bond yield increases, the mortgage rates offered by banks increase.

See below chart for the close correlation of the 10 year bond yield and the 30 year fixed rate mortgage rate.

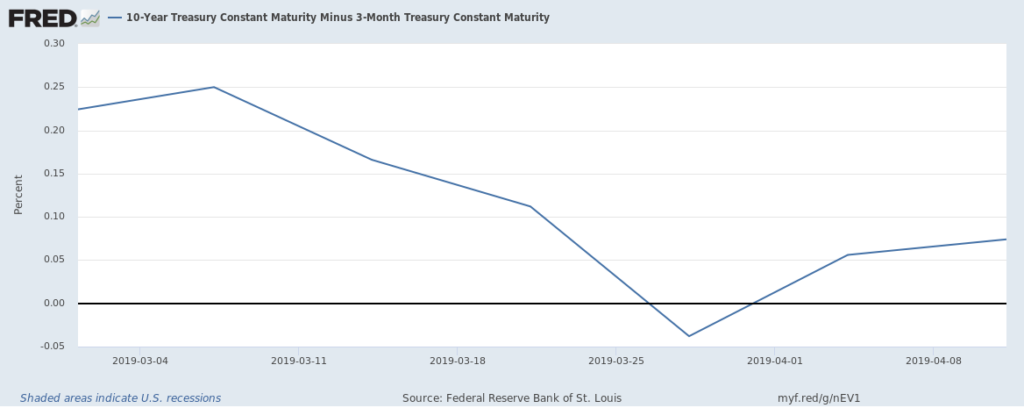

With the recent inversion of the 10 year bond curve (this means the 10 year bond rate is actually lower than the 3 month rate), it is a good time to think about refinancing your mortgage.

You can see on the graph below that the spread between the 10 year treasury and the 3 month treasury went negative in late March 2019. This made refinancing to a lower rate during that time very inexpensive. It can also mean that the current mortgage rate offered by banks might be lower than your existing mortgage rate.

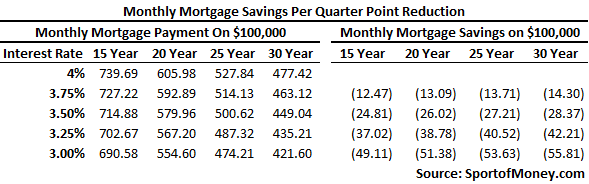

Refinancing to a lower interest rate is a good way to lower your monthly mortgage payments. The chart below shows how much you can save per month on a $100,000 mortgage if you lower the rate by 0.25%.

At times, banks might actually even offer to cover your closing costs if you refinance with them. Then, it really becomes a no-brainer to refinance your mortgage. If the closings costs are rebated back to you at closing, then the only investments you have to make are time and energy to (a) shop for the best available rate and (b) gather the necessary paperwork to go through the bank’s underwriting process.

Now is that time and energy worth the lower mortgage payment each month? You are the only person who can answer that question but, hopefully, the answer is a resounding YES.

Way #2: Extend The Mortgage Timing

Even if the mortgage interest rate is unchanged from when you first took out the mortgage, you can still lower your monthly mortgage payment by extending the mortgage timing.

Instead of having a 15 year fixed mortgage, you can refinance your mortgage to get a 30 year fixed mortgage. This will lower your monthly mortgage payment by $260 for every $100,000 in borrowing assuming a mortgage rate of 4%.

While your monthly mortgage payments will decrease, the total payment will increase if you extend the maturity. Instead of paying off your mortgage in let’s say 15 years, you will now pay off your mortgage in 30 years. You will have to make 360 monthly payments instead of 180 monthly payments.

This will result in a total higher amount of interest paid to the bank. However, it isn’t as bad as you think given the time value of money. The buying power of $1,000 in 30 years will likely be a lot less than today.

But obviously, this is the trade-off for reducing your current monthly mortgage payments by extending the mortgage payoff date.

Way #3: Refinance To An Interest Only Mortgage

Here’s another option to reduce your monthly mortgage rate. I personally do not recommend an interest only mortgage. But if this post is to inform you of different ways to lower your monthly mortgage payments, then this is definitely one option.

You can refinance your mortgage to be an interest only mortgage. In a typical mortgage, the monthly payment amount is allocated between principal and interest. A portion of the monthly payment is applied to interest on the mortgage and a portion is applied to principal. The principal balance gets reduced with each mortgage payment.

In an interest only mortgage, the monthly mortgage payment comprises of only the interest payment. No principal payment is included in the monthly payments. Therefore, the principal balance will not be reduced with each payment.

This can be useful for first time home buyers who might need liquidity early in the mortgage. This might also be beneficial for an investor who wants to conserve cash for another potential deal.

Way #4: Pay Down The Principal Balance And Then Recast

A sizable pay down of your mortgage principal balance is great if you suddenly come into a windfall or have recently sold off some assets and are sitting on a pile of cash. Even after a sizable principal pay down, if you don’t take any more action, your monthly mortgage payment amount will still remain the same. You will only reduce the total number of monthly payments to be made in the future.

What you can do if you want to lower your current monthly mortgage payments after a big principal pay down is to recast the mortgage. There could be a small recast fee charged by the bank. My bank charged me $200 to go through the paperwork of a recast for one of my mortgages.

What a recast accomplishes is to take your new principal balance, and amortizes that amount over the remaining life of the mortgage. Your original monthly mortgage payment amount was calculated based off of a higher principal balance. With a recast, the bank takes your current principal balance and recalculates the monthly payment amount necessary to pay off the principal and interest with the remaining payment schedule.

Way #5: Trade Down In Property Value

This option can cause a little disruption in your life but is also another way to lower your monthly mortgage payment amount. You can always sell the existing property you have and buy something less expensive.

On a less expensive property, your mortgage balance should be a smaller amount. The lower mortgage balance should result in a lower monthly mortgage amount as well.

This is one option that is good for empty nesters looking to downsize in both space and monthly expense payments. It can also be good for people re-locating from a high cost city to a lower cost city.

Spend less on the next house and your monthly mortgage payments will follow suit.

Way #6: Pursue Other Financing Options Outside Of Just A Mortgage

You can look to pursue another financing option in addition to just a mortgage. You might have access to a lower cost of capital such as from your prime broker, HELOC provider, or just borrowing from your parents. Don’t be afraid to utilize other forms of financing to help with the house purchase.

I used a cheap source of funds in borrowing from my prime broker to acquire an investment property. Instead of going through the mortgage process, I decided to draw cash out from Interactive Brokers.

At the time, Interactive Brokers was charging approximately 1% on the margin borrowing. That was 3.50% lower than the mortgage rate. Additionally, there was no monthly principal payment schedule necessary. Interactive Brokers would debit my account monthly for only the interest payment. Additionally, there is no origination fee or other fees associated with obtaining a mortgage.

This approach kept my monthly payments low. However, it does not come without risk. If you are borrowing on margin and the equity market drops significantly, you might face a margin call. You need to make sure you have sufficient market value in your prime brokerage account to take a significant drop in the market and not have to face a margin call.

A 30 year mortgage will probably give you a better peace of mind. But once again, if the goal is to lower your current monthly mortgage payments, looking for cheaper financing outside of a typical mortgage might make sense.

Way #7: Re-calculate Escrow Amount

The bank includes your escrow amount in your monthly payments. They want to ensure their collateral, your house, is well protected.

The monthly escrow amount typically includes payments for both homeowners insurance and real estate tax. The bank wants to make sure you are paying the homeowners insurance timely and that there is insurance coverage on the house.

The last thing the bank wants is for insurance coverage to lapse and then something terrible happens to your house that might lower or destroy the value of the house. The risk level of the mortgage increases if the collateral value deteriorates.

Real estate tax is another item the bank wants to ensure you are also paying timely. Local jurisdictions can place a lien on your property for late real estate tax payments. They might even be able to auction off your property. This is also dangerous for the banks as their collateral on the mortgage (your house) is at risk.

Review your escrow account to make sure the bank is calculating the right amount each month. If the bank is calculating too high of an amount, give the bank a call to get the escrow amount adjusted. This can help reduce your monthly mortgage payments to the bank.

Way #8: Shop For Lower Homeowners Insurance

Homeowners insurance, as previously mentioned, is included in the escrow payment you send to the bank as part of your mortgage payment.

Make sure to review your insurance coverage and talk to your insurance agent to ensure you understand what you are paying for and the coverage provided. If there is coverage you don’t need or some information is off with the insurance carrier, be sure to have them adjusted/correctly.

Don’t hesitate to also call up a few insurance agents for the best rate. Shopping around can help reduce your insurance premium.

I was chatting with a couple of people recently about home ownership. We came across the topic of homeowners insurance and I told them I was paying $3,000 a year on one of my investment properties. They mentioned, based on their own expenses, I was paying too much. I went back to my insurance broker and asked them to see if they can get me a better price.

Lo and behold, a week later, I was able to obtain a policy with a new insurance carrier with better personal liability coverage for $2,000. It was nice to be able to get better coverage for $1,000 less a year.

Reducing your homeowners insurance premium will result in the lowering of your monthly mortgage bill.

Way #9: Challenge Real Estate Tax Assessment

Another way to reduce your monthly mortgage payments is to reduce your real estate tax amount. Review the assessment report to see if your property’s market value or assessment is overstated.

If the real estate tax assessment seems too high, do not hesitate to challenge it. I have, in the past, hired a real estate tax assessment attorney to help challenge a real estate tax assessment. He didn’t get paid unless he can get me a lower amount. His fee was 30% of the real estate tax savings for the year.

This is a win-win situation. He gets paid only if he can reduce my real estate tax. If he can’t reduce the real estate tax, there is no money out of my pocket for his services. Now remember, your real estate tax doesn’t just get reduced for this year. The basis for the increase next year is also lowered. This will have a multi-year savings effect.

Lower your real estate tax assessment to reduce your monthly mortgage payments.

Way #10: Get Rid Of PMI

If you are currently paying PMI, try to get rid of the PMI payment. Pay down more of your principal balance to get it to be under 80% of the total value of your house.

Additionally, if you believe your house appreciated in value, you can get the market value re-appraised. Hopefully, with your re-appraised value, your loan balance will be under 80% of the new value.

Get rid of your PMI to reduce your monthly mortgage payments.

To the audience: What are some other ways for you to lower your monthly mortgage payments I didn’t capture above? Is mortgage payment one of your biggest expenses?

Many people work hard to better their physical and mental health. What about their financial health?

I started this blog back in 2019 to help people better their financial health as well.

My financial journey began with tens of thousands in student loan debt. Over the span of 20 years, I am close to achieving financial independence.

I truly believe anyone can get to strong financial health. Hopefully, this blog can help you on your financial journey to greater wealth and financial independence.

You can read more about me here.

Thank you for visiting. Come again soon!