How did Warren Buffett achieve his great wealth?

One of the tricks he employed was the mastery of “using other people’s money.”

He did this in a couple of ways. First, he started an investment vehicle with limited partners as investors in the vehicle.

Armed with cash from other people, he was able to go out and make investments or acquire businesses.

Secondly, even more powerful to Buffett, was the ability to obtain financing cheaply and then invest the proceeds at a significantly higher rate of return.

He was able to do this through the purchase of an insurance company, GEICO.

GEICO Provided Warren Buffett With A Cash Flow Stream

I’m sure you have seen all the GEICO commercials on TV. They are very memorable with the green gecko as their mascot.

GEICO provides insurance. They are probably best known as a car insurance company to the general public.

In fact, I have GEICO car insurance as well (as an aside, I thought their claims processing department was great when processing my claim).

GEICO is a subsidiary of Warren Buffett’s Berkshire Hathaway.

Maybe what is less known to the public is how much value GEICO has provided to Warren Buffett.

As an insurance company, GEICO collects premiums from its customers. It’s liability in return is the potential pay-out of claims on those insurance policies.

A sophisticated operation with a long history and actuarial models, GEICO can calculate how much pay-out they can reasonably assume to have based on all the insurance policies they have sold.

The pay-out happens further down the line. A driver pays the insurance premium up front. Maybe a month or 2 in, the driver gets into an accident. The claim is processed and, ultimately, paid out. That process takes time.

But in the meantime, the insurance company has usage of the cash premium to make investments. The cash premium received but has not been paid out in a claim is called the float.

Using The Power Of The Float

A simplistic example to illustrate how the float works:

GEICO charges $1,000 on an insurance policy knowing that there is a high likelihood GEICO would have to pay out $900 one year in the future.

Obviously, GEICO is in the business to make money. Therefore, there is a $100 profit on that policy for GEICO (the difference between the premium and the future pay out).

To enhance the profit, GEICO would then invest the $1,000 into Apple stock. Apple goes up $200 during that year.

Instead of GEICO making just $100 from that policy, GEICO has now increased their profit to $300 given the increase in the price of Apple stock.

Warren Buffett uses the float (the insurance premium received) to make investments.

Because of his investment prowess, his investments returned a substantial sum, far and above the claims paid out.

That is how Buffett was able to use other people’s money to enhance his own net worth and the value of his companies.

How can you become a mini-Warren Buffett?

Utilize Other People’s Money To Enhance Your Own Financial Position

Just as how Warren Buffett used the float from GEICO to make investments which out earned the cost of the money, you too can also utilize other people’s money to enhance your own financial position.

In my mind, one of the easiest ways of having access to other people’s money is by obtaining a mortgage on a real estate purchase.

The federal government of the United States wants homeownership to continue to grow. After all, isn’t owning a home part of the American dream?

They have made ownership easier by providing incentives to the banks to make mortgages to home buyers. The banks can in essence offload the risk related to the mortgages to government backed entities.

I find it is to our great advantage, as investors, to have this source of financing available.

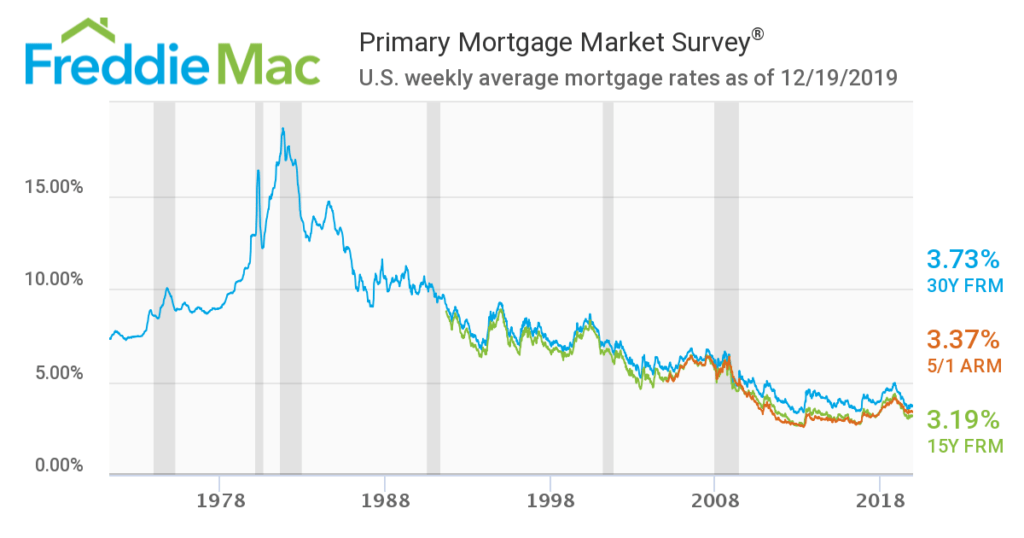

Now, the mortgage is influenced by treasury rates. Treasury rates are at an historical low.

Therefore, mortgage rates are at an historic low. See graph below.

I will show you how you can take advantage of this unique opportunity at this time in the market to help increase your net worth.

Of course, with the use of financing, if real estate prices move up, the return is greater. But on the flip side, if real estate prices drop, the pain and loss gets multiplied.

It is up to each of us individually to determine if the opportunity outlined here works or not.

I believe it presents a great opportunity for wealth creation and I am trying to acquire as many rental properties as possible as long as access to mortgage remains cheap.

Why I Like Real Estate

Anyone who follows this blog knows I am a big fan of real estate. I’ve written a number of articles about why I believe real estate should be the cornerstone of any investment portfolio.

Some of the advantages of real estate include:

Ability To Buy Below Market

Given each real estate deal is individually negotiated; there are opportunities to be able to acquire real estate at below market value.

I’ve written a blog post on how to buy real estate at below market price.

Ability To Add Value

It is an asset class which offers the ability for you to increase the value of the asset based on your own action.

If you buy an Apple stock or bond, unless you acquire enough to have a say in the company, you are a truly passive investor.

There is little you can do to add value to your stock or bond holding. You basically end up going where the market takes you.

That is not entirely the case with real estate investments. Of course, when the real estate market tanks, there will be negative effect on the property.

But you also have opportunities to add value to your real estate property from renovating it to getting better renters.

You can even challenge the real estate tax assessment value to lower your real estate tax bill.

There are many opportunities to increase the value of your real estate investment for someone who is ambitious in maximizing value and doesn’t mind putting in the time and financial resources to get it done.

Tax Benefits

Gains are taxed at the preferential long term rate when the property is held longer than a year. You can sell a real estate investment property and buy a new property tax free (assuming you meet the rules) in a 1031 exchange.

The best tax benefit for me is that you can deduct non-cash expenses to lower the amount of taxable rental income. This allowed me to generate over $400,000 of rental income and not pay any income taxes.

The Power Of Cheap Financing

Now that I’ve highlighted why real estate is such an attractive asset class, let’s see how we can use the current environment of low mortgage rate to our advantage.

No different than how an insurance company can make money by using the float; you can take advantage of the low mortgage rate offered by your bank to increase your return profile.

The math works out the same.

Imagine if I tell you that you can borrow at a 3 percent interest rate and then you can invest that money to generate a 5.5 percent return, would you want to borrow as much money as possible?

I know I would.

The difference between your borrowing rate and your investment return is 2.5% in this example. That is profit you can just pocket.

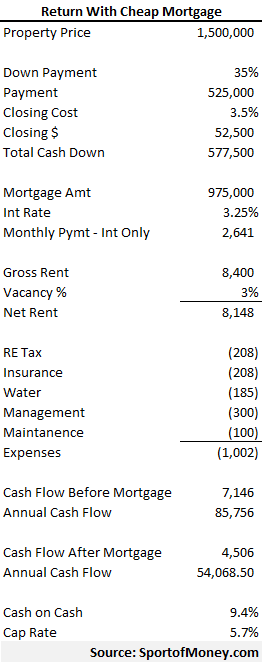

Let’s examine how by taking advantage of the low mortgage rate offered by a bank has helped me increase the return of my investment:

Without the cheap mortgage, the return on the investment would not be as attractive (5.7% versus 9.4%). With the cheap mortgage rate, sign me up all day long on that investment opportunity.

Why I Like Interest Only Mortgage For Rental Properties

When I applied for a refinancing of an existing mortgage for a rental property recently, the bank gave me the pricing and the terms of the mortgage.

It was 3.25% for a 10/1 ARM with $2,000 back at closing to help offset closing costs. I though the rate was good and went ahead with the mortgage.

Lo and behold, it turned out to be an interest only mortgage. I didn’t have a lot of experience with interest only beforehand and was a bit skeptical if it’s a good option for me.

The biggest difference between an interest only mortgage and an amortizing one is that there is no principal pay down associated with each monthly payment in an interest only mortgage.

That means, after 10 years of making mortgage payments, the principal outstanding is still the same amount owed when the mortgage was taken out.

At first, it didn’t sound good to me.

But when I did a bit more research on interest only and spoken to a few people, I actually like interest only mortgage a lot more than the normal mortgage for a rental property.

The interest only mortgage gives me a greater cash flow.

If no principal payment is required on a monthly basis, there is less of a mortgage payment to make. That increases the cash flow from a rental property to me.

Who wouldn’t want a greater cash flow?

Additionally, there is an option each month to make a principal payment if I so choose without penalty. Therefore, if I want to effectively turn it into a normal amortizing loan, I have the ability to do so.

Now, you might ask who wouldn’t want an interest only. Generally, interest only loans can have a higher interest rate. But in my case, the bank only offered interest only for a rental property.

Now that you see the impact to return of using a mortgage with a cheap rate, let’s examine some tips I’ve used to obtain a lower mortgage rate.

How To Get A Lower Mortgage Rate

Shop Around For A Mortgage

This tip is quite obvious and can apply to any type of purchases. Shop around.

If you want to obtain the best interest rate with the best terms, you have to talk to a number of lenders to figure out who can offer you the best interest rate and terms.

Ask around and talk to people you know such as co-workers, neighbors or friends and family members to see if people can provide you with contacts at lenders they have used before.

Use the internet to look up the advertised rates offered by different lenders.

In order to obtain the best rate, you need to spend the time to do the research to see who offers the best.

Don’t Hesitate To Negotiate The Interest Rates And Other Terms

Once you have shopped around, you now have a sense as to what is offered out there in the market place.

Some lenders might have better terms when it comes to interest rates, others might have better closing cost rebates, and others might not have an application fee.

Settle on a lender or two which have some of the preferential terms. If there are some terms which are not the best you have gotten from other lenders, do not hesitate to negotiate with that lender to see if you can obtain the better terms as well.

For instance, if you go to 6 lenders and one of them comes back with the best rate of 3% instead of 3.25% from the other 5 lenders. But this one lender has an application fee of $1,000 as opposed to the other lenders with no application fees.

You should negotiate with that lender which offered the 3% interest rate and let that lender know that no one else is charging an application fee and you would like to get that fee waived.

In order to get the best rate and terms, you have to negotiate with the lenders.

Move Assets To The Bank

A lot of banks out there want to establish not only a mortgage lending relationship with their customers but other relationships as well such as banking or wealth management.

If you have a pool of assets such as cash or listed stocks and bonds, utilize that to your advantage

Banks have promotions in which you might be able to reduce your interest rate by up to 1 percent depending on how much assets you can transfer in to the brokerage arm of the bank.

I’ve used a bank a few times now which offered a quarter percentage point reduction in interest rate on $500,000 of assets deposited with the bank, half a percentage point reduction on $1 million deposited and 1 percent reduction on $2 million deposited.

That quote of 3% interest rate can drop even lower when you factor in the ability to move assets to a bank.

Take Advantage Of Promotions/Specials

Be on the constant look out for promotions or specials from lenders.

You know the price difference between buying a microwave at retail price versus when buying one when it is on a cyber-Monday sale. The savings can be enormous.

Believe it or not, banks can also run promotions or specials when providing a mortgage. You can save money when you take advantage of a promotion or special.

I’ve taken out a home equity line of credit (HELOC) when the bank was running a special. I didn’t have to pay any fees to obtain the HELOC. Even the appraisal fee was covered for me.

Additionally, the bank offered a very low introductory rate for the first year of the HELOC.

Of course, it made plenty of sense for me to obtain the HELOC given I didn’t need to pay anything upfront for the ability to borrow money whenever I need it.

And if I need to borrow for the first year, I would pay a very low interest rate.

Does that sound like a no brainer to you? It wouldn’t be hard to see that I took action and got the HELOC.

To The Audience: Do you like real estate as an asset class? What, if any, is your hesitation with buying an investment property with a mortgage? Have you obtain mortgage pricing back from a lender recently? If yes, what are the terms and interest rate?

Related Posts

Are You Struggling To Achieve Your Financial Goals? Here Are Ways To Stack Success In Your Favor.

Anyone Can Be Wealthy In America – Are You?

Small Action – Big Financial Impact

Many people work hard to better their physical and mental health. What about their financial health?

I started this blog back in 2019 to help people better their financial health as well.

My financial journey began with tens of thousands in student loan debt. Over the span of 20 years, I am close to achieving financial independence.

I truly believe anyone can get to strong financial health. Hopefully, this blog can help you on your financial journey to greater wealth and financial independence.

You can read more about me here.

Thank you for visiting. Come again soon!