I’m an infant when it comes to my personal finance blogging career. I really started SportofMoney.com in earnest earlier this year. But even in my short time spent on the blogging circuit, I’ve come across quite a few like-minded bloggers and a common concern shared by us: there is not enough financial literacy among Americans.

I wrote a post recently titled “The 9 Reasons Why The Rich Keep Getting Richer.” I don’t think it is a secret that it becomes easier to make money when you have money. The game is stacked incredibly in your favor when you are rich. Take for instance, a 10% return on $10,000 produces $1,000. Nothing to sneeze at; but apply that same 10% return on $10,000,000. Now we are really cooking!

Making Money Is A Game

Making money is really a game. Those people who understand the rules do very well. Those who have no clue how to play will find it very hard to win. And those people who don’t realize that a game is being played will be out of luck.

Michael from Financially Alert captured this best when he commented on the post:

“…the rich have figured out the rules to the “game” when most people don’t even realize there’s a game being played. (It’s hard to win a game if you don’t know the rules!)”

Financial Literacy Provides Cheat Code For The Game Of Money

Financial literacy provides you the cheat code on the rules to help play the game better. I aim to play to win. You should too and being educated more about personal finance will go a long way in helping you build wealth.

There is a financial illiteracy crisis in America. Nearly 2/3 of Americans cannot pass a 5 question test about basic financial literacy from FINRA Investor Education Foundation. 63% of Americans got three or fewer answers correct out of five questions. You can try the test for yourself by clicking here.

One way of combating this is to educate our youth about the game, and the rules of the game.

Mr. Hobo Millionaire lamented in one of his comments:

“It’s a real shame basic investing (like a Vanguard index fund) is not taught to everyone while in school. $100/month invested from age 20 to 65 will grow to ~1M (and we all know you can add more than $100/month as you get older). There is simply no reason why more people don’t have large amounts of savings — they just don’t know the “game” (ie. math).”

We are taught history, art, music and science at grade school. However, there no classes which educate our youth about personal finance.

That is why I was positivity surprised when I came across this article about how one high school is teaching hundreds of students how to become millionaires.

High School Program Teaches Students To Become Millionaires

In a Philadelphia neighborhood where many parents don’t have a bank account, an educator named Dan LaSalle started a financial literacy program in 2015 at a high school. The program itself not only teaches students about “the importance of budgeting, saving and investing, but also gives them the opportunity to get paid up to $5,000 a year, and to put that money into a bank account of their own.”

Students are given the option to make between $50 and $5,000 by working at the school during the school year. The jobs range from teaching to tutoring to running clubs at the school. Dan LaSalle also helped the students in opening up savings and checking accounts. Some students even have brokerage accounts to invest in stocks.

“The goal is that everyone in the class will be a millionaire at some time in their life,” LaSalle says.

A Great Start

The students are up to a great start on their journey to greater financial knowledge and freedom. I have little doubt that if the students stick to the program and use the knowledge and experience obtained, they will be millionaires at some time in their lives.

At least they are far ahead of where I was during their age. I worked part time in high school as a senior but I didn’t open a savings or checking account until I was 18. I didn’t open up a brokerage account until I was in college. Those kids are certainly ahead of where I was at their point in life.

It is also great to see an educator be devoted to educating students about financial literacy. Dan LaSalle is currently the assistant principal of that high school. He was an English teacher when he started the program. Hopefully, he can continue to progress in his career and could exert greater influence over more and more schools to implement his program.

I don’t think there is a better way to educate the young about money than to have them actually practice the materials taught in class.

Financial Benefit Of An Early Start

Compounding is a wonder of the financial world. Compounding has the greatest impact the longer time you allow the money to grow. This is one way I grew my 401(k) balance into over $1,000,000 before the age of 40. I started putting money into my 401(k) account when I started working full time at the age of 22. My wife started at the same age and also has over $1,000,000 in her 401(k) account in her 30s.

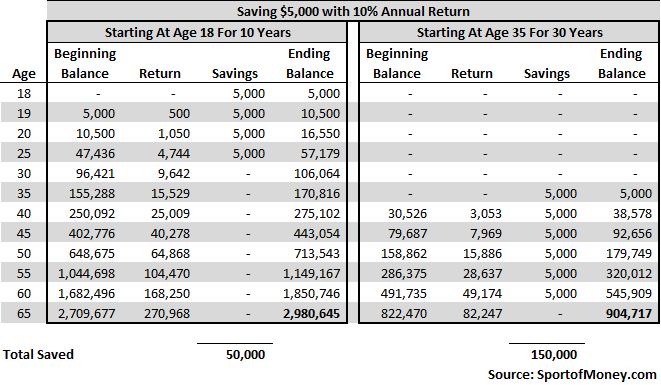

Just starting early can produce great results. Let the power of compounding work in your favor by maximizing the time horizon. Below is an example which shows the magic of compounding.

On the left hand side, Person A contributed $5,000 per year starting at the age of 18 over a 10 year span. Person A stopped the contribution at the age of 27 for a total contributed amount of $50,000. Person B, on the right hand side, started contributing $5,000 at the age of 35 for a 30 year span. Person B stopped the contribution at age 65 resulting in a total contribution amount of $150,000.

As you can see from the table above, Person A ended with a balance of close to $3,000,000 by the age of 65 assuming a 10% annual return. Persona B ended with a balance of less than $1,000,000 by the age of 65 also assuming a 10% annual return.

Despite Person B having contributed 3 times the total amount when compared to Person A, Person B ended up with less than 1/3 of the amount saved by 65 than Person A. Wow, isn’t the power of compounding great!

This hopefully highlights to you the power of an early start.

Lessons To Teach Young Kids

The article laid out a few steps we can teach our kids before the age of 18 to provide them with the best opportunity to reach financial independence one day. Maybe they can grow up to be millionaires as well. I have no doubt that if our kids do the below, our kids will grow up to be significantly better off financially.

Here is how we can apply some of the ideas the high school is doing to raise financially independence kids to hopefully be millionaires one day.

Provide Our Kids With Financial Education

As previously mentioned, about 2/3 of Americans cannot answer basic questions about financial literacy. Please make sure it doesn’t happen to your kid. Educate your kid about financial literacy as early as possible.

There are many ways to help educate your kid about the basics of finance. You can google “teaching kids about money” and find over 300,000,000 results ranging from audio guides to books to games to charts.

Try to start early with the financial education lessons. I have 3 young kids under the age of 8. I try to incorporate financial lessons into our conversations when the situations present themselves.

They have accompanied me a few times to my rental properties. I’ve explained to them why I have rental properties, what I provide to my tenants (shelter/home) and what my tenants provide to me in return (rent).

I believe it is never too early to start educating kids about finance and money. Like the great power of compound return, I believe the earlier you can educate your kid about finance, the greater return the kid will have in the long run.

Allow Our Kids To Earn Money

Just as I believe it is never too early to expose kids to financial concepts, it is also a great idea to allow our kids to take action. Explain to them the virtue of work and the reasons for work. Once they have an understanding of these two concepts and are old enough, allow your kids the latitude to go out and earn money.

Earning money is the first step along the path of becoming a millionaire and in generating wealth. Whenever I watch Shark Tank with the kids, and I see young teenage entrepreneurs pitch their businesses to the sharks, I would always mention to my kids that it is never too early to start a business by pointing to those young entrepreneurs as examples.

Encourage Our Kids To Budget And Save

After your kid brings home the first paycheck, encourage your kid to save. Only by saving can the kid really accumulate wealth. It doesn’t matter how much the kid earns, if the kid spends the pay immediately, then the kid will end up with nothing.

The article mentions a way to encourage kids to save. Help your kid open up a checking or a savings account. Explain to your kid the difference between the two. Have your kid deposit money into the account immediately after each payment date.

Additionally, help the kid set a budget and a target savings amount. This way, you can have a particular savings goal for the kid to hit.

You can help set the budget and the savings by walking the kid through how much money will be made from the job, what the after tax amount will be, what the kid can then use the money to buy and how much the kid has left in the checking or savings account after taxes and spending.

Encourage Our Kids To Invest

Earning money and saving the money by themselves are not enough. Our kids need to earn how to invest the money in order for it to generate even more money. Let the power of compounding turbocharge the savings.

Without investing the money, the savings will only decrease in buying power given inflation. Open up a brokerage account for your kid. Teach your kid the various options for investment such as a bond investment versus equity.

Some of the brokerage accounts have a planning for retirement module. Encourage your kid to run various retirement simulations of what the savings will look in 40 to 50 years given different types of investments. Then tell your kid to put the savings into an investment, monitor the investment periodically, and watch it grow over the years.

There are other ways to invest the money besides a brokerage account. You can also encourage your kid to invest the money into starting a business or being a partner in a real estate venture. The key is to have the kid not be afraid or hesitant to invest the money.

It’s Easy To Become A Millionaire When Starting Young

It really doesn’t take much if you start young to be a millionaire. Saving $5,000 from the age of 18 to 21 (a total over the 4 years of $20,000 without contributing another cent after) can result in over a $1,000,000 by the age of 61 with a 10% annual return. A 10% return is approximately the historical average annual return for the S&P 500.

To the audience: Are there other ways to help kids along the right financial literacy path? What have you done with your kids which worked well you would like to share with the readers here? How did you do on the financial literacy quiz?

Many people work hard to better their physical and mental health. What about their financial health?

I started this blog back in 2019 to help people better their financial health as well.

My financial journey began with tens of thousands in student loan debt. Over the span of 20 years, I am close to achieving financial independence.

I truly believe anyone can get to strong financial health. Hopefully, this blog can help you on your financial journey to greater wealth and financial independence.

You can read more about me here.

Thank you for visiting. Come again soon!

My parents did not make big money as a salesman and a school teacher but they became millionaires by being frugal, not to mention they had pensions that covered their retirement costs so their investments just grew and grew. They were open about their finances and the extreme giving they practiced and my brother and I adopted their strategies and became multimillionaires ourselves. A lot of life turns out the way you predict it will for yourself. We saw average earnering parents become wealthy and we expected as gifted STEM majors to do even better than our folks, and we have. Part of generational wealth is living up to your own expectations for yourself. They also made sure we had jobs outside our home from our preteens through the rest of our lives. That’s not easy to do now but there weren’t any enforced labor laws back then! Having role models in your home is pretty huge.

You are fortunate to have such great financial role models.

I try hard to impart financial lessons on my kids with the hope of them doing better than my wife and me one day.

“Part of generational wealth is living up to your own expectations for yourself.” – I like this part. I hope parents can instill in their kids high expectations for themselves.

Agree with all of this! My wife plays in the sport of teaching : ).

She is a math teacher and this year actually brought in two local bankers to present some of these concepts to the kids. She thought it would be more impactful coming from an outsider rather than her just teaching it through her normal lesson planning. She got great feedback from the kids! Have a good Tuesday!

Oh – and I got 6/6 on the quiz. Woot!

Nice! You are part of the knowledgeable 1/3.

It’s nice to hear your wife brought in two local bankers to discuss financial concepts with the kids. Nothing beats getting information from people who live and breathe the topic. It is also great to hear the kids enjoyed the lesson and provided positive feedback.

Do other teachers in her school also provide some financial literacy education to the students in the school?

I don’t get the impression other teachers do – we recently moved to a rural area so it just isn’t part of the focus unfortunately.

My partner and I recently talked about how wonderful it’d be if we’d started saving and investing at 8, instead of 22 like most people after graduating college. I like that you brought your kids to your rental properties. What a great way to introduce them to real estate! I wish I’d received lessons like that when I was little. Curious which of these were most fun to learn for your kids?

My kids are still very young (all under 8). I’m not sure if they have fun but they are definitely curious. When I started discussing rental properties with them they asked a lot of questions (like why do people rent from you, who owns the property, etc).

I think they really had fun one night when, after a bed time story, I asked them how they would go about building a success business running a pizzeria. Their imagination really went off about different product offerings and ways to attract customers.

Great post, Rich! Don’t forget about the game of Monopoly! I played it so much as a kid. As silly as it sounds, it helps with quick math, adding/subtracting in your head, just being comfortable with money.

And compounding (combined with broad stock market investing)… the grand poobah of money. It’s like magic. It’s IS magic. Charts like the one you posted are 100% correct, but unbelievable.

Many of us make the dumbest financial decisions between 18 and 28. If we could simply avoid those decisions and save, the math is life changing. I know “kids” need to learn independence, but when you see a chart like the one you posted, you could almost make an argument for “kids” NOT leaving home until 28. Yes, get educated and go to work, but save tons of money until 28. Then move out, you can stop saving, and your retirement years are already funded. It’s crazy!

Good stuff.

I agree with you that there is a very compelling financial case to be made to live at home (if job opportunities are available) for at least a few years right after college. I was able to do that (although not up to the age of 28) and it really provided me a great financial start. I was able to save up a down payment for my first home that way.

I can’t wait for the youngest to be old enough to play Monopoly. Now it gets hard to play because the youngest would want to participate but would end up disrupting the game.

I second the monopoly recommendation. I started playing that with my grandpa as a young kid and I helped spark an interest of money and making/saving/investing money.

Love this! One thing we did is purchase a 3D printer as a family Christmas gift. My son always has ideas that involve building and the printer helps him bring his ideas to life. As he gets older he is starting to think of ways to use it for a business.

To be able to turn a hobby into extra money is nice, especially if he can establish an ongoing business from it.